To fight inflation, measure it better

For several months now, rising prices have dominated public consciousness and raised anxiety in most households. Not for decades has Statistics Canada’s monthly inflation rate indicator been awaited with such rapt attention. This indicator is much like a thermometer monitoring the fever of a patient under observation.

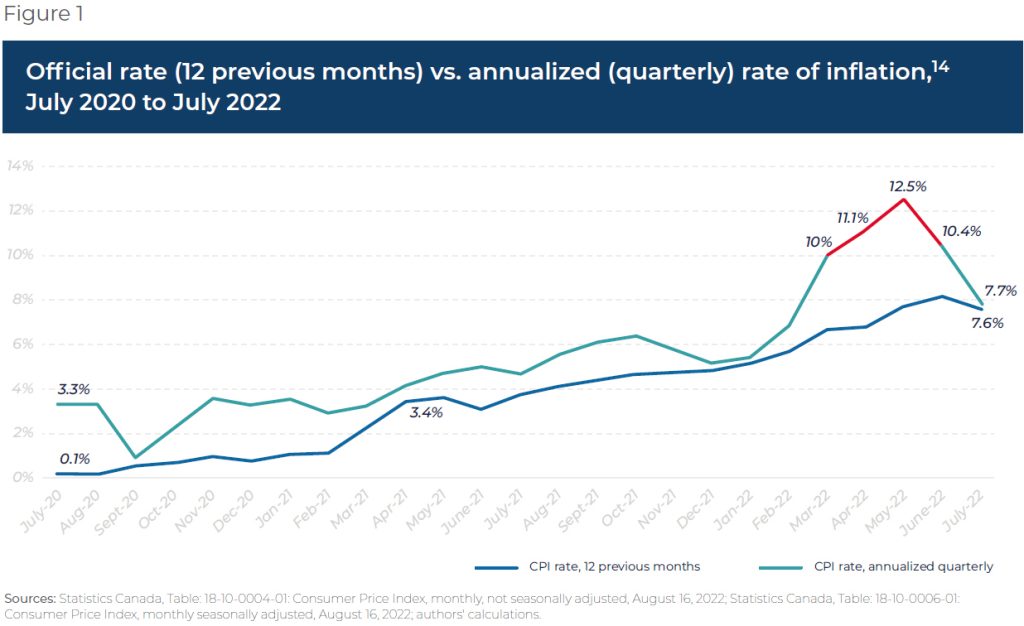

The most recent data show the rate of price increases slowing down, from 8.1% in June to 7.6% in July. But the reality perceived by consumers is markedly different. So how do we explain this disconnect?

What appears paradoxical, in reality is not. The explanation for this lies in the calculation methods employed by Statistics Canada. The public agency measures the official inflation rate based on the change in the Consumer Price Index (CPI) over the past 12 months. This is how it can state, for example, that the CPI has increased by 7.6% year-over-year. This is what we can call the “retrospective” (backward-looking) rate of price inflation, a rate that is firmly rooted in the past.

However, since this rate calculates the loss of purchasing power already recorded over the past year, it provides very limited information on the inflation we are experiencing at the moment, the rate we are suffering under right now, or even, for example, over the past month or quarter.

Consider the following analogy. Since the official rate is retrospective, it is like knowing the average speed at which a car has travelled over the course of the last hour. This data allows us to measure the distance travelled during that hour, but it tells us nothing at all about the car’s current speed. Is the car travelling at 50 km/h, 80 km/h or 120 km/h? Has it stopped? The average speed over the last hour cannot answer these questions. It is therefore of little use in predicting the distance that will be travelled in the next hour if the current speed is maintained.

This is why we should be much more concerned with the prospective (forward-looking) inflation rate, which is derived by looking at changes in the CPI. This figure, and not the one in the headlines, has far more potential to reveal what’s in store for us. It is also important to note that this forward-looking rate is not a recent invention — Statistics Canada itself was publishing it right up until 2007!

By focusing on the prospective rate, we could have discerned the first signs that inflation was exceeding the 2% objective in July of 2020, almost a full year before official statistics showed any deviation from the target rate. Worse still, the prospective rate was in double digits last May, at 12.5%, before it fell back below 10% in July.

This prospective rate therefore represents a very different way of looking at inflation, one that turns out to be far more reflective of Canadians’ lived experience. Using such information, monetary authorities could have corrected their policies much more quickly and thus more effectively combatted the erosion of Canadians’ purchasing power.

Nathalie Elgrably-Lévy is a Senior Economist at the MEI and Valentin Petkantchin is Vice President, Research at the MEI. They are the authors of “For a Better CPI Indicator in Canada” and the views reflected in this opinion piece are their own.