The State of Competition in Canada’s Telecommunications Industry – 2018

The criticism most often heard regarding the telecommunications industry in Canada, and especially wireless services, is that Canadians pay a lot more than people in other countries for lower quality services. It is this criticism that was used to justify the federal government’s and the CRTC’s numerous interventions over the past few years aimed at promoting more competition in the wireless sector. But does this criticism stand up under scrutiny?

Media release: Canadian wireless prices competitive, despite simplistic comparisons

Previous editions: 2017 / 2016 / 2015 / 2014

Related Content

Related Content

|

|

|

| Happy 50th, CRTC. You can stop now (National Post, May 8, 2018) | Interview (in French) with Martin Masse (100% Normandeau, BLVD 102.1 FM, May 8, 2018)

Interview (in French) with Martin Masse (Phare Ouest, CBUF-FM, May 8, 2018) |

Interview with Martin Masse (The Close, BNN Bloomberg, May 8, 2018) |

The 2018 edition of The State of Competition in Canada’s Telecommunications Industry was prepared by Martin Masse, Senior Writer and Editor at the MEI.

Highlights

The 2017 edition of this report argued that the Internet of Things, which will revolutionize every aspect of our lives, will soon force Ottawa to reconsider its telecommunications priorities and policies. It also analyzed some issues that had made headlines in the industry over the previous year, and looked back at the 2006 Policy Direction telling the CRTC to rely on market forces as much as possible. Here are some highlights from this year’s edition.

Chapter 1 − How Does Canada Measure Up?

- Canadians continue to enjoy competitive, quality telecommunications services.

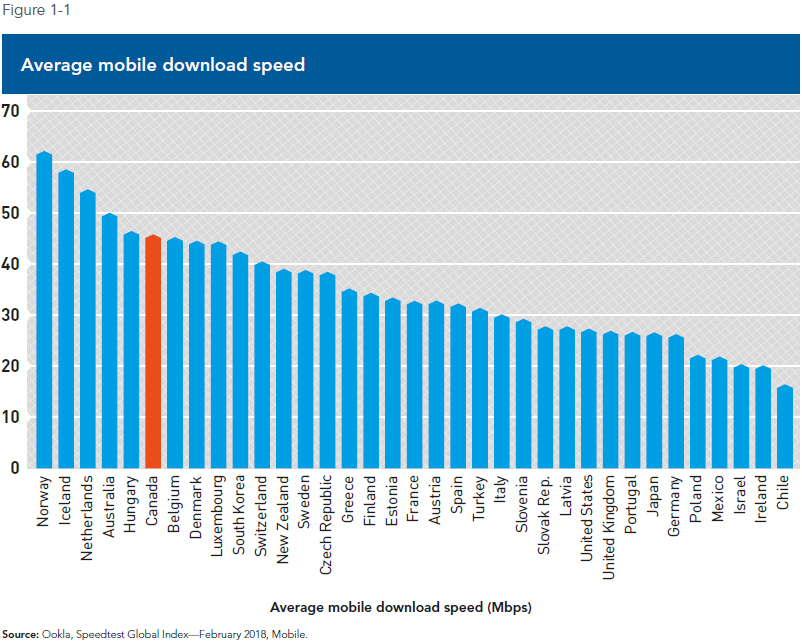

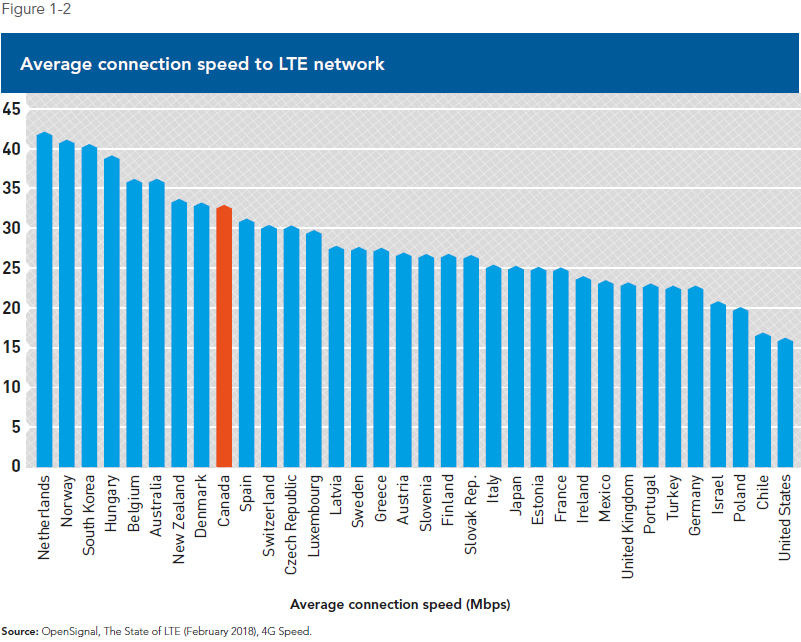

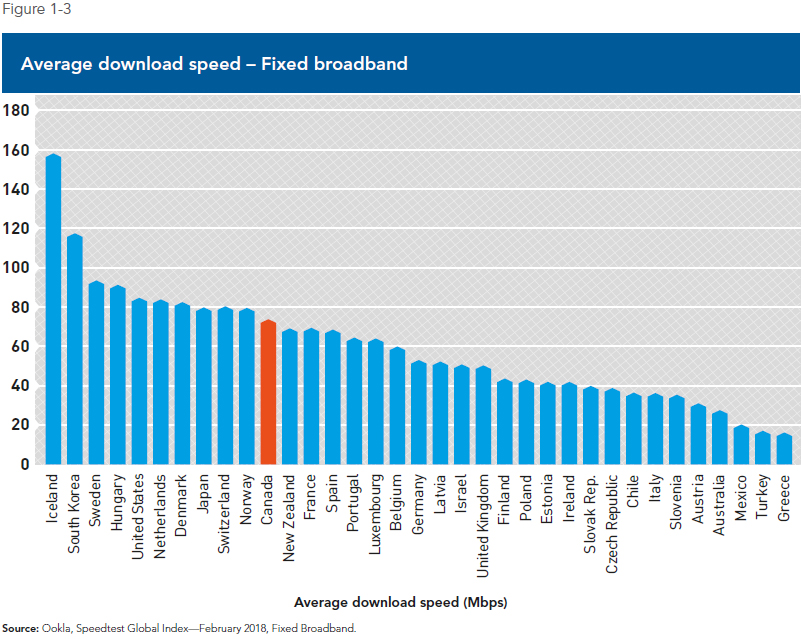

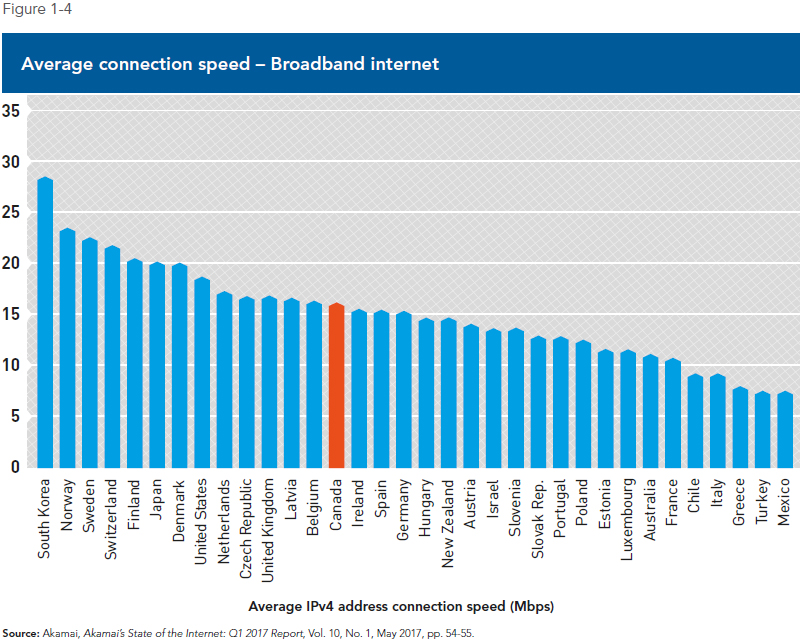

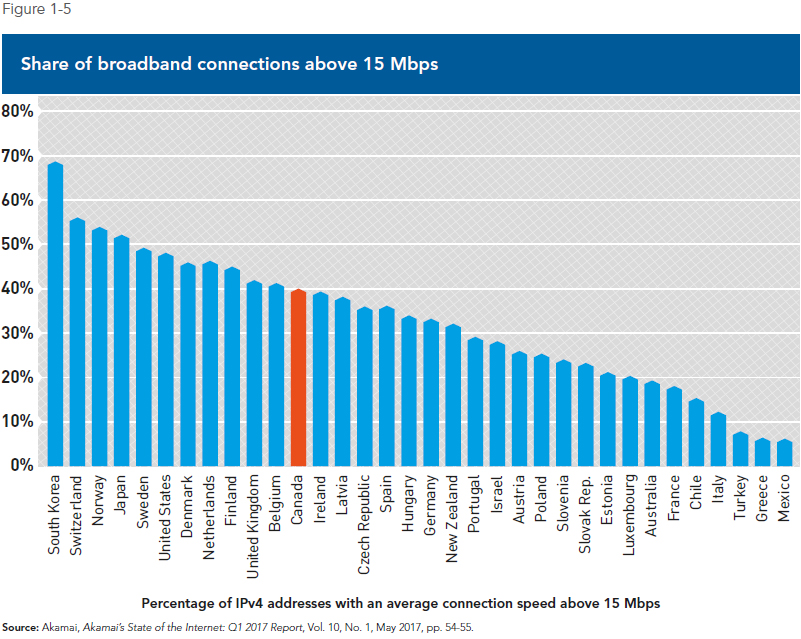

- Thanks to some of the most advanced and efficient wireless and broadband internet services in the world, download and connection speeds in Canada compare very favourably with speeds in other OECD countries.

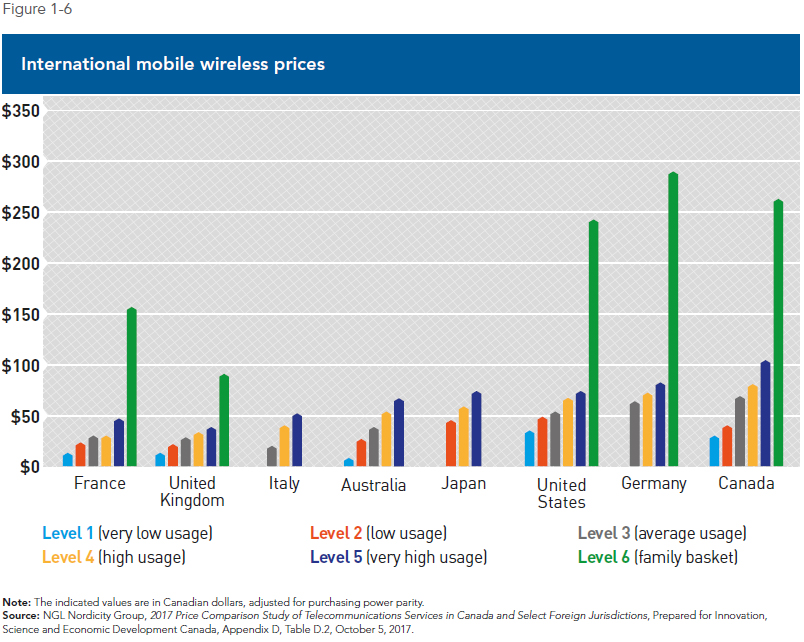

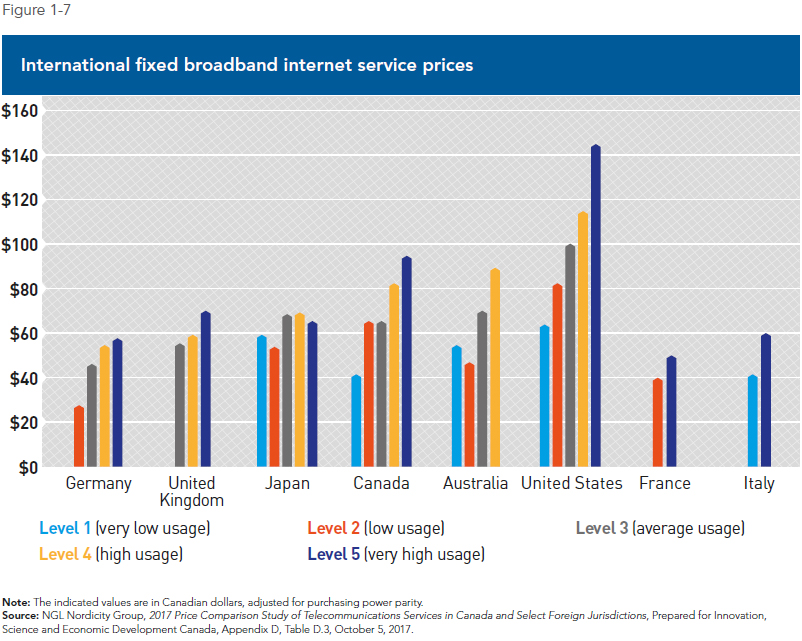

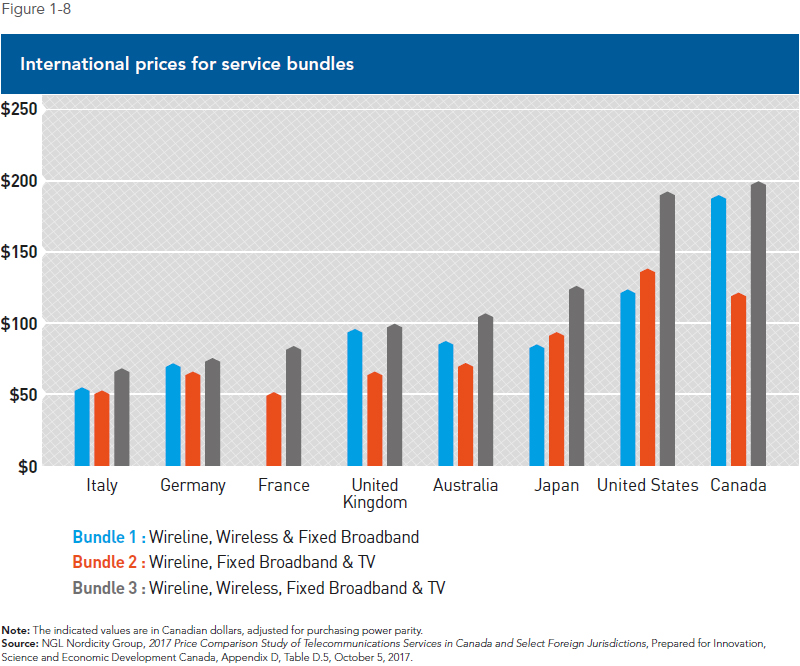

- The prices Canadians pay for telecommunications services according to Nordicity’s international comparisons remain generally higher than in most countries.

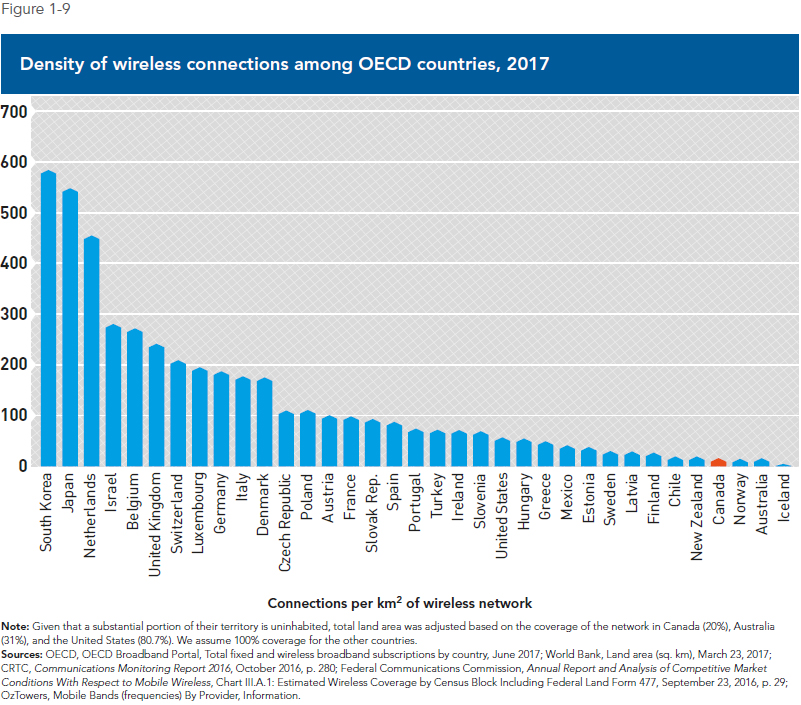

- Canada’s density of wireless connections per km2 is one of the lowest in the world.

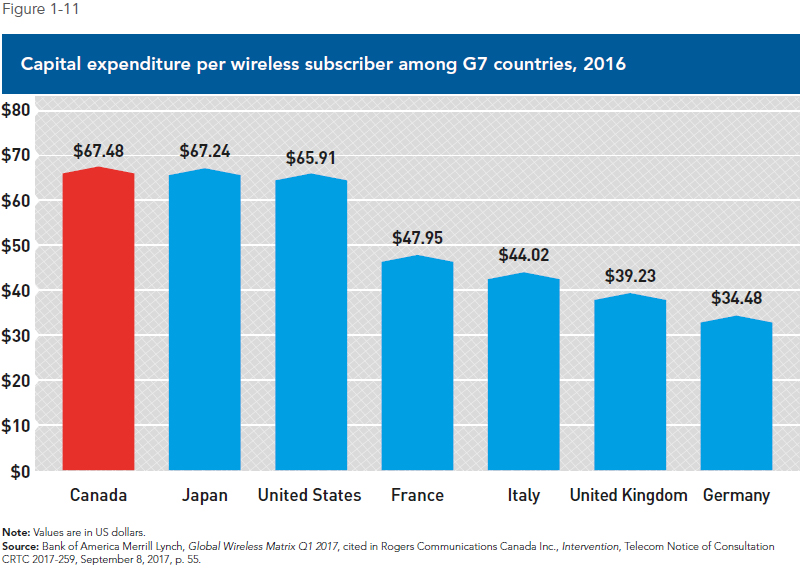

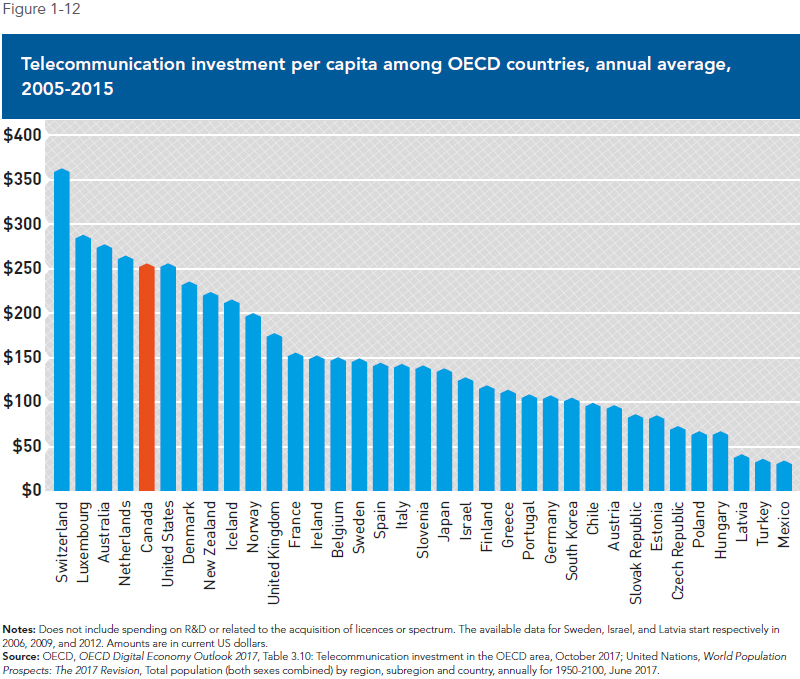

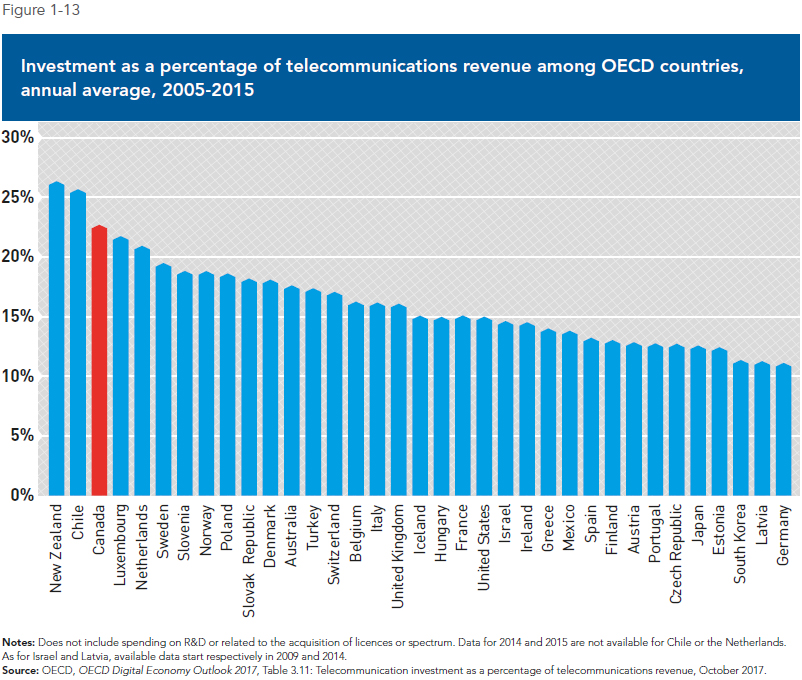

- In terms of telecommunications companies’ investment, Canada outshines most other countries, whether measured per wireless connection, per wireless subscriber, per capita, or as a percentage of revenues.

Chapter 2 − Are Canadian Telecom Prices Really among the Highest in the World?

- Despite a widely shared perception, the available data do not support the conclusion that Canadians pay significantly higher prices for telecommunications services than consumers in other developed countries.

- The Nordicity study upon which this perception is based compares prices for general categories of products, but ignores most factors that explain how these products and the markets where they are produced and sold are different.

- International metrics have consistently shown that Canada has some of the highest quality wireless networks in the world.

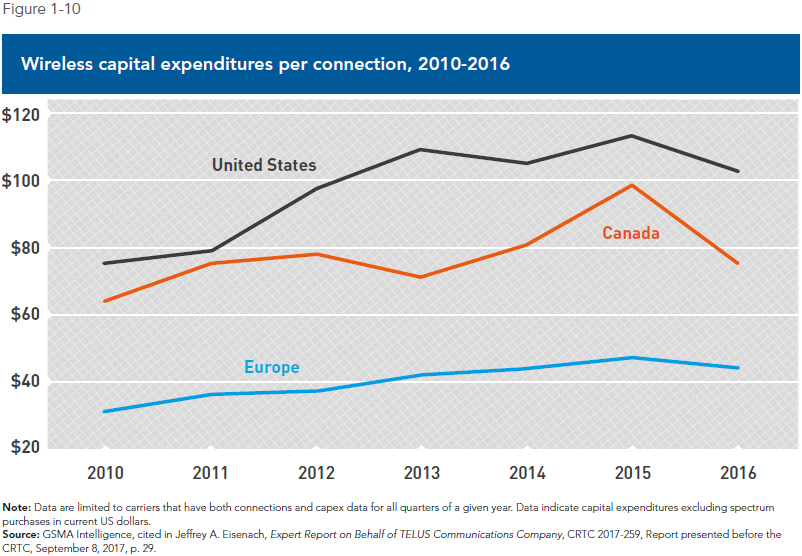

- Wireless carriers in Canada invested on average US$78 per connection between 2010 and 2016, almost twice as much as their European counterparts, which only invested $40.

- Canadians are heavy users of telecommunications services, and they’re paying for world-class networks that can deliver the fast, reliable, high-quality services they expect.

- Nordicity’s limited set of data hides the simple reality that Canadians have many more affordable options: They can get similar service baskets at cheaper prices by switching either to a flanker brand, a regional provider, or a reseller.

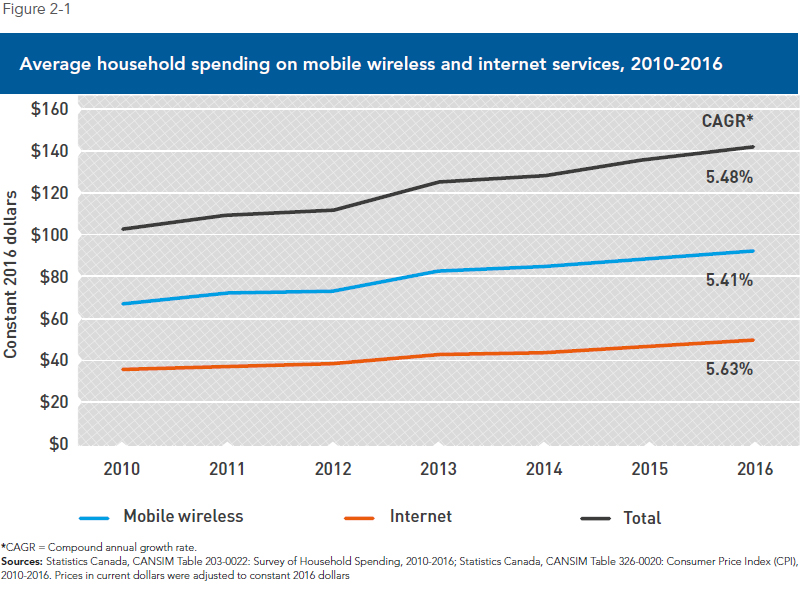

- The average bill that Canadians pay for their wireless and internet services keeps increasing not because they have to pay more for the same services, but because they are paying more for more and better services.

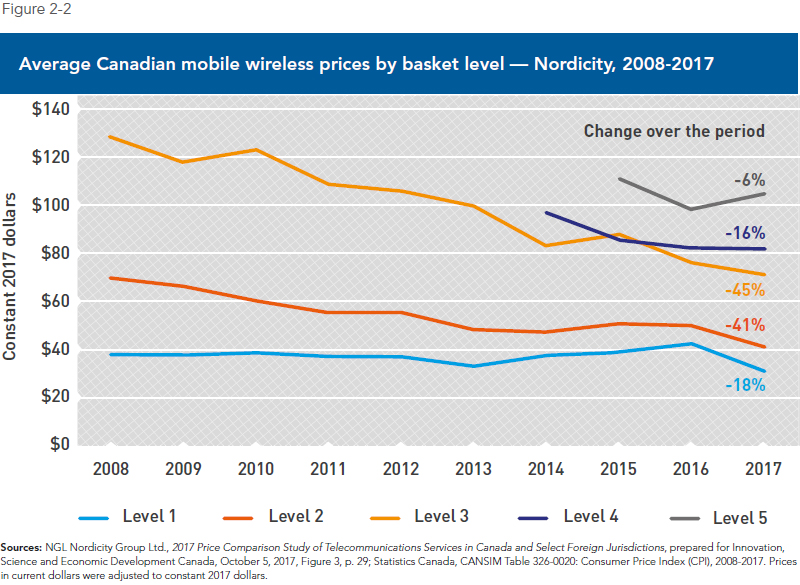

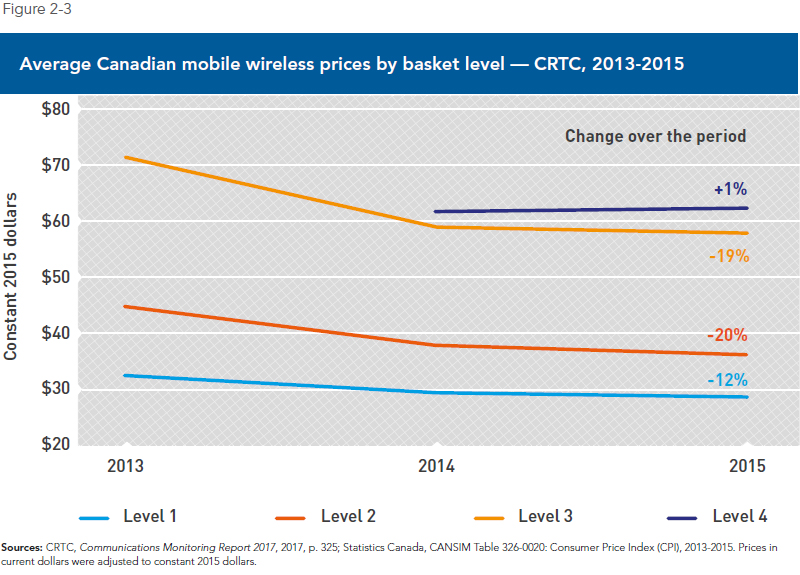

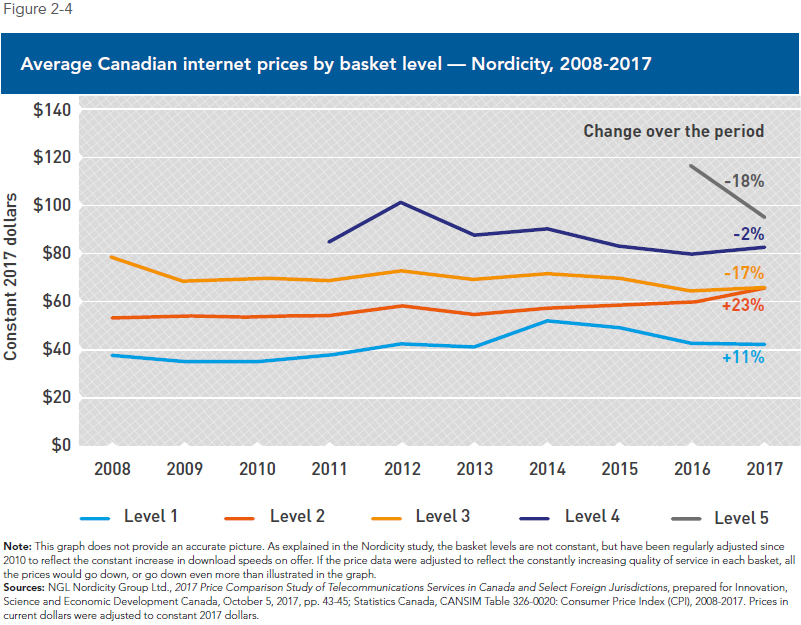

- Adjusted for inflation, the prices for wireless telephony service baskets have all gone down between 2008 and 2017, with reductions of from 6% to 45%.

Chapter 3 − Broadband Regulation: Should Canada Emulate the United States?

- The telecommunications sector in the United States has been buzzing with controversy since November 2017, when Ajit Pai, the recently appointed chairman of the FCC, announced his proposal—approved in December—to do away with the stricter “net neutrality” rules introduced in 2015.

- Although critics have used dramatic terms to characterize the repeal of Title II regulation, it merely reverts back to the lighter-touch regime that governed the internet from 1996 to 2015.

- Broadband network investment had fallen more than 5.6% since the FCC’s 2015 net-neutrality decision, the first such decline outside of a recessionary period.

- Despite the repeal of the Open Internet Order, every major U.S. internet provider supports prohibitions against blocking, throttling, and unfair discrimination.

- The main concrete difference so far between the FCC’s and the CRTC’s approaches to net neutrality has been the steadfast opposition of the Canadian regulator to zero-rating.

- In banning innovative and pro-competitive targeted pricing plans, the CRTC has not protected the integrity of the internet; rather, it has raised prices for certain consumers and lowered prices for no one.

- A 2016 study found that fibre-to-the-premises coverage in the United States was approximately double what it was in Europe, and overall next-generation access coverage was 82% in the U.S. compared to 54% in Europe.

- The CRTC should revisit its 2015 decision to give resellers access to high-speed networks, and phase out its broadband network sharing regimes, as the United States did in the early 2000s.

Chapter 4 − We No Longer Need a Telecommunications Regulator

- Over the years, the CRTC has shifted its attention from the retail side of the telecommunications market to the wholesale side, where it has implemented a variety of interventionist policies aimed at helping new entrants and resellers.

- Since Canada has successfully transitioned from monopoly to competition, there is a case to be made that the CRTC should be phased out as Canada’s telecommunications regulator.

- Network sharing policies, initially adopted to stimulate competition in wireline telephony, failed to create facilities-based competition in Canada, and if anything undermined new entrants’ incentives to build alternative facilities.

- Facilities-based competition, in wireline telephony and in the broadband internet market, was able to flourish in Canada thanks to the cable industry, not as a result of network sharing policies.

- The Wireless Code’s two-year contract provision, far from being “pro-consumer,” has reduced choice and limited the ability of carriers to develop innovative customer offerings.

- In its Final Report published in March 2006, the Telecommunications Policy Review Panel found that “the Canadian telecommunications industry has evolved to the point […] where detailed, prescriptive regulation is no longer needed in many areas.”

- The Danish experience with light-touch regulation, in particular the deregulation of its wholesale wireless market, should serve as a source of inspiration for Canada.

Introduction

For each of the past four years, The State of Competition in Canada’s Telecommunications Industry has assessed how Canada measured up with other jurisdictions regarding the quality and pricing of its telecommunications services. The report has also evaluated how competition was faring in key areas of the Canadian telecommunications market, and provided a critical assessment of Canada’s legislative and regulatory framework for this industry.

One of the primary motivations for the publication of the first four editions of this Research Paper was that many Canadians appear to be under the mistaken impression that Canada’s telecommunications industry compares poorly with that of other jurisdictions.

This report has attempted to dispel the notion that Canadians pay uncompetitive prices for low quality services. It has also argued that the federal government’s and the CRTC’s interventions in the wireless and wireline sectors aiming to increase the number of players through indirect subsidies and mandated access were not likely to have the intended effects and might jeopardize investments and innovation. This is all the more important given the burgeoning Internet of Things, since only large, facilities-based competitors will be able to make the necessary investments in networks and manage those networks to answer the complex needs of this new sector.

This report has argued that the government should instead liberalize its policies and recognize the role of innovation in assessing the level of competition that exists in a dynamic market.

This fifth edition continues to explore these themes. Chapter 1 provides updated statistics regarding the performance of the Canadian telecommunications industry compared with other jurisdictions.

Chapter 2 provides a more in-depth analysis of the issue of pricing than has been offered in previous editions, explaining why the data contained in the annual Nordicity study fail to support the common perception that Canadian telecom prices are excessive and ever increasing.

Chapter 3 compares broadband internet regulation in Canada and the United States, looking at recent changes to net neutrality rules south of the border and Canada’s continuing opposition to zero-rating, as well as the CRTC’s 2015 decision to force broadband providers to share fibre-to-the-home broadband networks with resellers.

Finally, Chapter 4 makes the case that since Canada has successfully transitioned from monopoly to competition, the CRTC should be phased out as Canada’s telecommunications regulator, and the sector should move to a general regime of competition law, like almost all other sectors of the economy.

The graphs (Click to enlarge)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|